🔥 Automatic expense categorisation is here! No more sorting invoices by hand.Show me →

English

English Čeština

Čeština Slovenčina

SlovenčinaBank reconciliation software for restaurants

Automated bank matching for restaurants and pubs: every supplier payment paired with its invoice, every POS deposit checked against the bank — built to sit alongside Xero and Sage, not replace them.

Schedule a demo

The hidden cost of manual bank reconciliation in restaurants

Bank reconciliation in a restaurant isn't just about matching the bank statement with transactions. It's threading sales, card processor settlements, delivery payouts and supplier payments from the same week — and finding the gaps before they cost you money.

Data not synced

POS reports on your sales today — but the bank deposit lands 2–4 days later less card processor fees.

Transactions get lost

Every supplier invoice has a corresponding bank payment somewhere — finding it takes hours.

Verifying takes forever

Delivery apps (Uber Eats, Deliveroo, Just Eat) settle weekly, less commission — almost impossible to verify line by line.

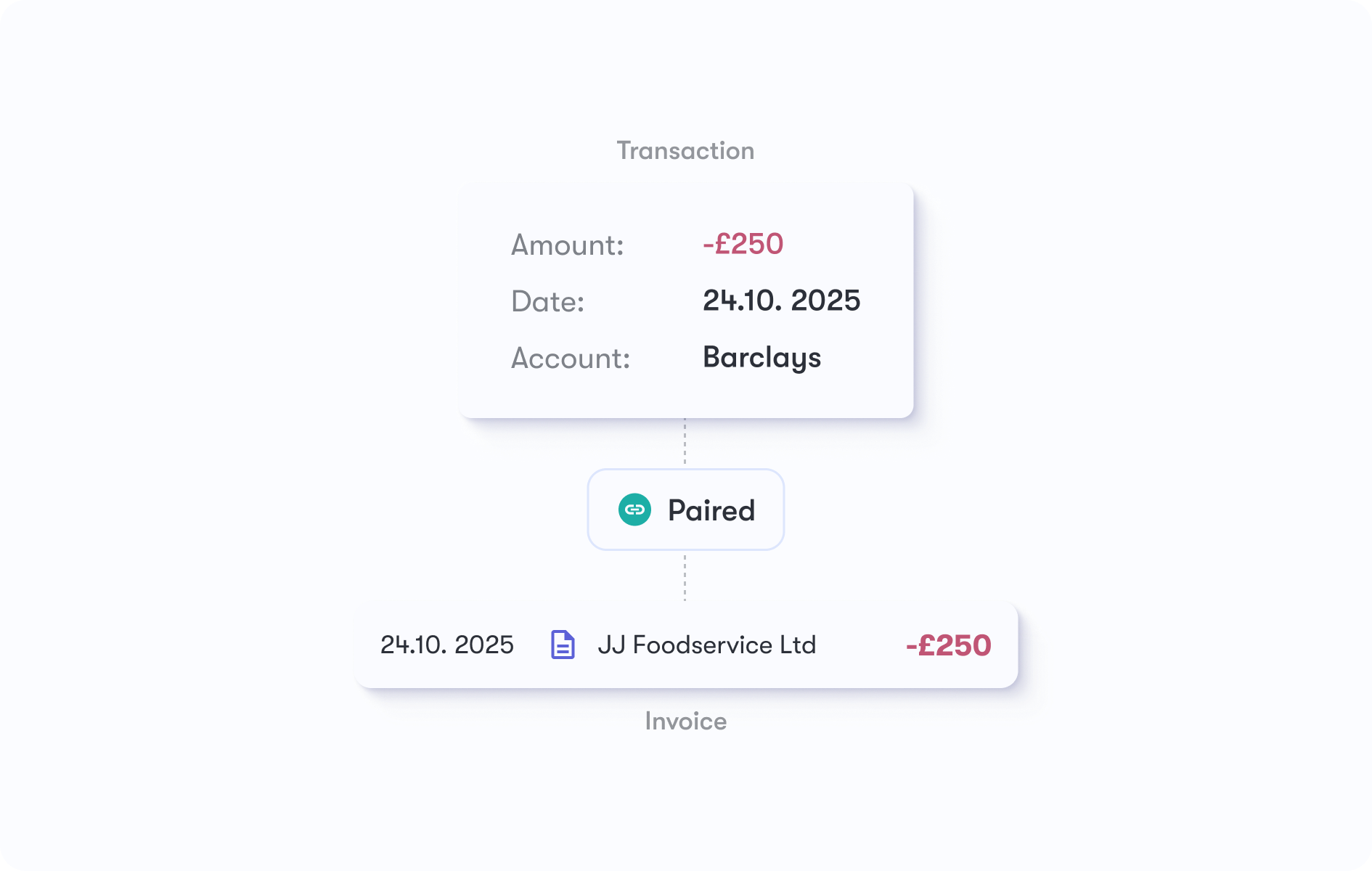

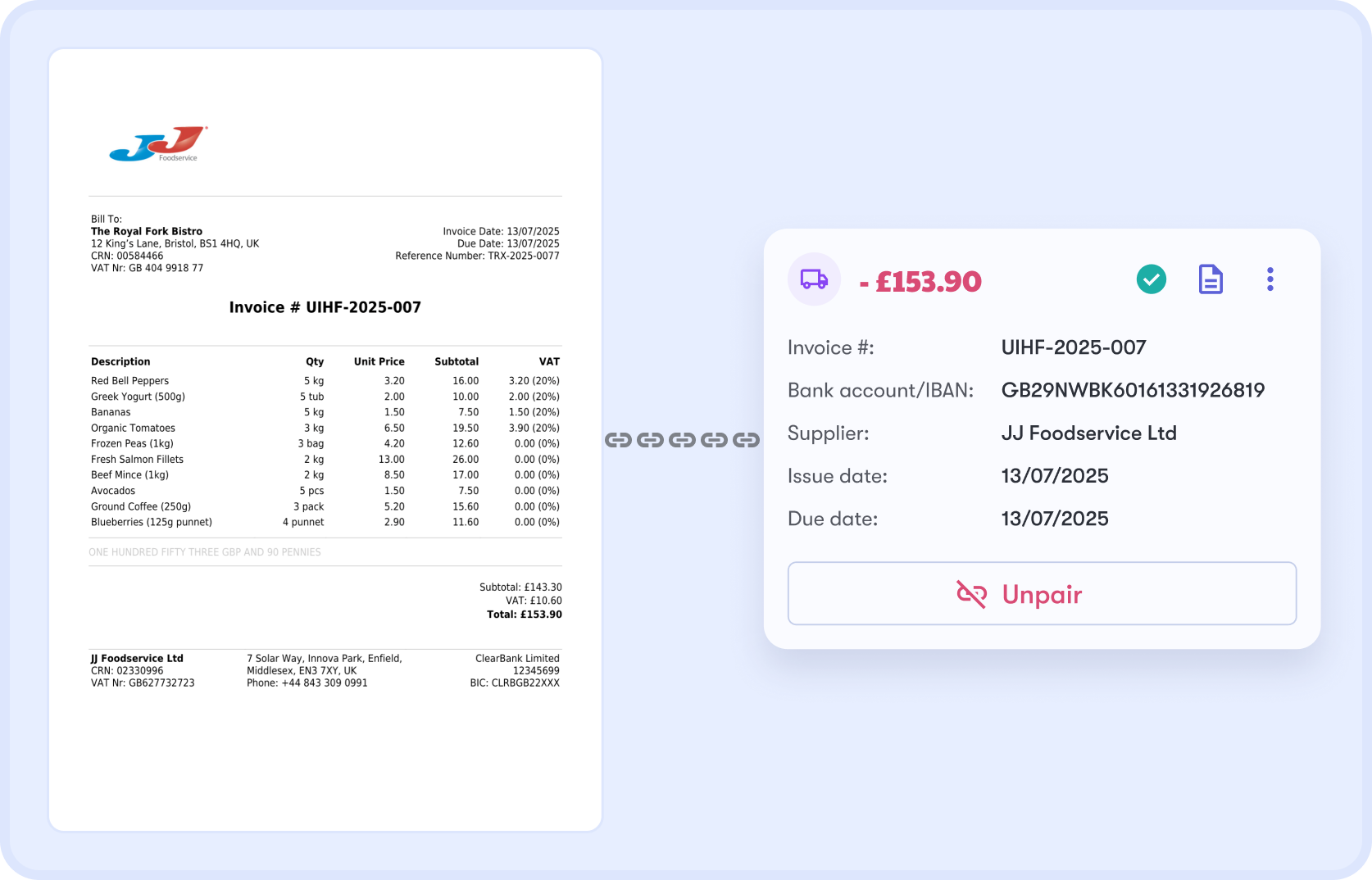

Automated bank matching — invoice with payment

Most accounting software matches your bank to a general ledger account. Dishboard matches it to the specific invoice — closing the accounts payable loop at line-item level, not just at category level. The result: you always know which payment cleared which supplier invoice, and what's still outstanding.

Live bank feed integration for UK restaurants

Direct banking connection in Dishboard— no CSV downloads, no PDF parsing, no manual import. Transactions flow into Dishboard as they clear, ready to match the same day.

POS deposits, card settlements, delivery payouts — all matched

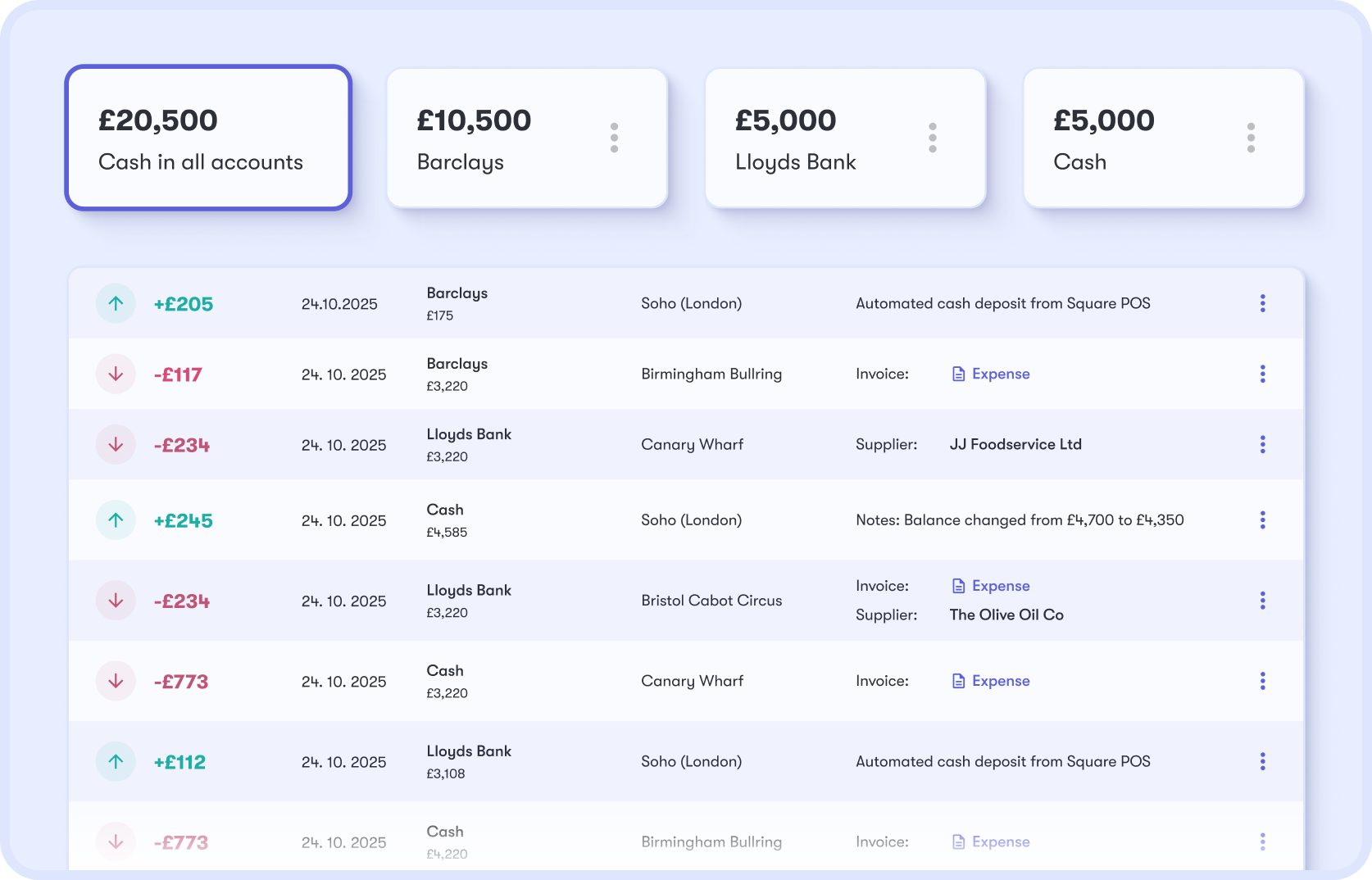

POS deposits, card processor batches, delivery app payouts and supplier payments all hit the bank on different schedules. Dishboard tracks each chain end to end — from till to bank — so payment reconciliation across hospitality channels stops being a manual job.

Streamlined reconciliation for all venues

For groups, multi-location bank reconciliation gets exponentially harder — more accounts, more processors, more delivery platforms, more suppliers per site. Dishboard rolls every venue into one ledger and lets you drill into any single transaction at any single site.

Built around your accountant — not a replacement for Xero or Sage

If you’re already on Xero or Sage, the question is fair: why add another tool? Because Xero and Sage match your bank to general ledger accounts. Dishboard matches it to the specific invoice — closing accounts payable at line-item level — then hands clean, matched data back to your books of record.

| Xero / Sage alone | Spreadsheet | |

|---|---|---|---|

| Matches bank to invoice line | Yes — automatic | Bank to GL only | Manual |

| Restaurant context (POS, delivery, tips) | Yes — built in | Generic | Manual |

| Time per month (10 sites) | Minutes | Days | Weeks |

How long should restaurant bank reconciliation take?

There’s no single “right” rec time, but the typical bands by venue size are remarkably consistent across UK hospitality. The table below sets industry expectations and shows where automated matching changes the math.

| Venue type | Manual rec time | With Dishboard | Recommended frequency |

|---|---|---|---|

| Single café / bistro | 2–3 hours/week | Minutes | Weekly |

| Pub (food + wet) | 4–5 hours/week | Minutes | Weekly |

| Casual dining (single) | 5–6 hours/week | Minutes | Weekly |

| Multi-site (3–10 venues) | 1–2 days/week | Minutes | Weekly per site |

| Restaurant group (10+) | 2–3 days/week | Minutes | Daily |

If your bank rec is taking more than 2 hours a week per single venue — or you’re doing it once a month — supplier payments, card lag and unmatched deposits are quietly piling up. Dishboard surfaces them as they happen, not at month-end.

Built for how UK hospitality actually pays and gets paid

Built around how UK venues actually move money — Open Banking under FCA, VAT on tips and tronc, HMRC-ready exports, and the POS systems operators here actually use.

Open Banking under FCA — read-only, secure, no card sharing

FCA-regulated read-only access — Dishboard sees your transactions, cannot move money, cannot initiate payments.

VAT on tips and tronc handled correctly — service charges separated from sales

Tronc and service charges stay separate from revenue, so VAT only applies to what's actually sales.

British English, £, HMRC-friendly export to your accountant

Reports come out in £ with line items mapped to the categories your accountant expects.

Works with UK POS: Square, Lightspeed, Epos Now, Toast, SumUp, Dojo

Direct integration with every major UK till — no exports, no middleware.

See how restaurants use Dishboard to stay profitable

How Beverley Hills Diner & Bar saved £1,300 and cut finance time by hours

How Pub Automat saves up to 35 hours per month and reduces ‘pour cost’ thanks to Dishboard

How Ive from Bistro Lagom Eliminated 15 Spreadsheets

Frequently Asked Questions

Bank reconciliation is the process of matching every transaction in your bank account to its source — supplier invoices, POS deposits, payroll runs, card processor settlements. In a restaurant the volume is high and the moving parts are more complex than a typical business: card payments lag the sale by days, delivery apps settle weekly net of commission, and supplier invoices can run into the hundreds per month.

Three things make it harder. Card sales hit the till today but the bank deposit lands two to four days later, net of processor fees. Delivery apps (Uber Eats, Deliveroo, Just Eat) pay weekly with commission already deducted. And the volume of small supplier payments — produce, drinks, cleaning, repairs — is far higher than most non-hospitality businesses ever deal with. Generic bank reconciliation tools weren't built for any of this.

Weekly is the minimum for a single venue, daily for groups of ten or more. Anything monthly means you're learning about supplier overpayments, missed deposits or processor errors a month after they happen — long after they're easy to fix. The benchmark table above shows typical times by venue size, both manual and with Dishboard.

No. Dishboard sits alongside Xero or Sage, not in their place. Your accountant still uses your accounting software as the books of record, files VAT, and runs year-end. Dishboard handles the heavy lifting on accounts payable and bank matching at line-item level — then sends clean, matched data into your accounting stack instead of raw transactions.

Dishboard tracks the full chain: POS gross sales today, processor batch net of fees over the next few days, then the bank deposit. Each stage is matched automatically, fees are split out, and you can see exactly when card revenue from a given shift will land. No more guessing whether yesterday's £1,840 in card sales will deposit as £1,802 on Wednesday.

Yes. Each delivery platform has its own settlement schedule and commission structure — typically weekly, net of commission, with separate handling for delivery fees and customer tips. Dishboard pulls the platform statements, matches the payout to the orders, separates commission from net revenue, and reconciles the deposit when it lands in your bank.

Tips paid to staff and service charges treated as tronc are separated from sales revenue, so VAT isn't charged on money that's passing through to the team. Dishboard keeps tronc payments visible for your payroll and HMRC reporting, but they don't pollute your sales lines or your VAT returns.

Open Banking is FCA-regulated and read-only by design. Dishboard sees your transactions but cannot move money, initiate payments, or change anything in your account. The connection is secured to UK banking standards, can be revoked from your bank app at any time, and never asks for your card details or password.

Yes. Each venue's bank account, deposits and supplier invoices sit in one ledger with per-site and group views. Drill down from group total to a single transaction at a single venue, catch site-level discrepancies before they hit the consolidated P&L, and export one reconciled set of figures for your accountant.

Ready to close the loop between your invoices and your bank?

It takes 20 minutes. We'll connect to your bank and POS in read-only mode and show you what's matched, what's not, and what's costing you time.

Schedule a demo